TL;DR:

- Leverage in property investing involves using borrowed money to control larger assets, amplifying both potential gains and risks. Proper understanding of metrics like LTV, ICR, and debt service coverage ratio is critical to managing leverage safely and scaling portfolios. Successful investors start conservatively, stress-test deals, and use refinancing strategically to grow without overextending financially.

Leverage in property investing is defined as using borrowed capital to control a larger asset than your cash alone would allow, amplifying both returns and risks relative to your equity contribution. A $300,000 rental property purchased with 20% down and 80% mortgage financing means your $60,000 controls a $300,000 asset. That is the core mechanic behind property investment leverage, and understanding it separates investors who scale portfolios from those who stall. Key tools in this framework include loan-to-value ratio (LTV), interest coverage ratio (ICR), and debt service coverage ratio (DSCR). This guide covers how leverage works mathematically, which metrics matter most, what financing types are available, and how to apply leverage strategies without overexposing your portfolio.

How does leverage amplify returns and risks in real estate investing?

Leverage multiplies your return on equity, but it multiplies losses by the same factor. That symmetry is what makes understanding property leverage non-negotiable before you deploy capital.

The math behind amplified returns

Consider two scenarios on a $400,000 property that appreciates 10% to $440,000. Investor A pays cash. Investor A earns a 10% return on $400,000 invested. Investor B puts down 25% ($100,000) and finances $300,000. Investor B earns $40,000 on $100,000 of equity, a 40% return before financing costs. That gap illustrates why leverage is the primary wealth-building mechanism in real estate investing explained at the institutional level.

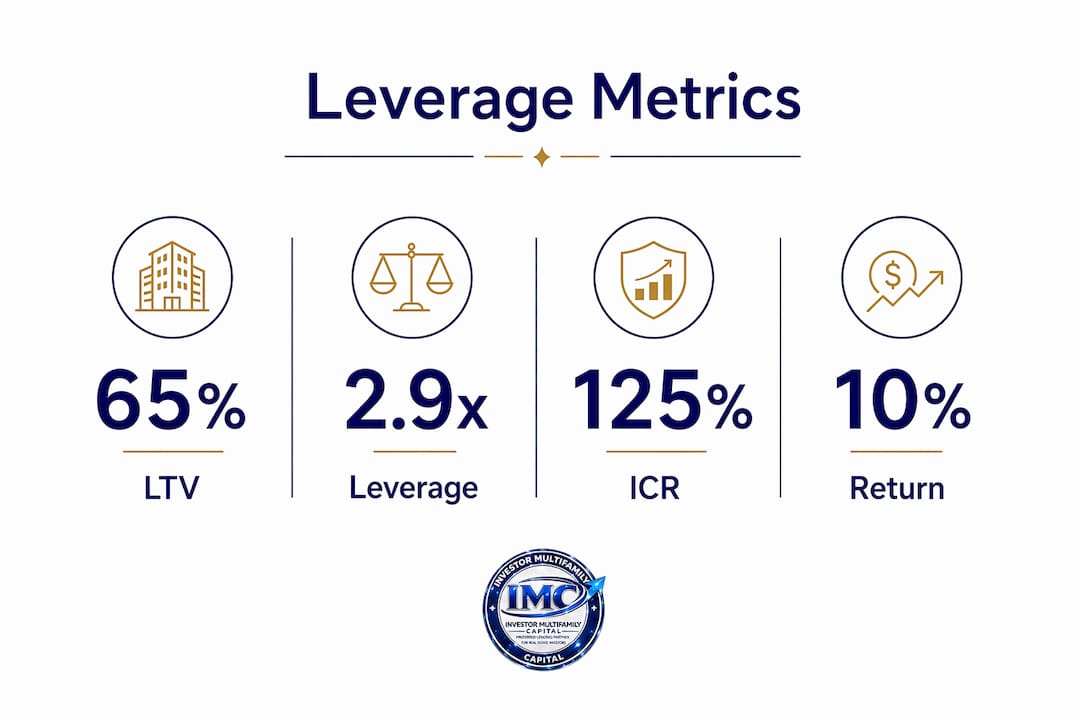

The leverage ratio formula makes this precise. Leverage ratio equals 1 divided by (1 minus LTV). At 65% LTV, the leverage ratio is approximately 2.86x, meaning each dollar of equity controls $2.86 of property value. At 80% LTV, that ratio jumps to 5x. Higher ratios amplify upside, but they compress your equity cushion against any decline.

Positive vs. negative leverage

Positive leverage exists when your property’s cap rate exceeds your borrowing cost. If a property yields 7% and your loan costs 5.5%, the spread works in your favor. Negative leverage occurs when financing costs exceed the property’s income yield, which destroys returns even when the property performs. Many investors in 2023 and 2024 discovered negative leverage firsthand as rates rose faster than rents. Monitoring this spread is a core discipline in leverage strategies in real estate.

Risk amplification is not theoretical

A 10% property market decline can cause a 50% equity loss when you hold 50% equity. That is not a worst-case scenario. It is arithmetic. The real danger is not paper losses but forced sales or refinancing under stress, when lenders tighten criteria and valuations fall simultaneously. Leverage redistributes risk rather than eliminating it, and the additional return from leverage compensates for that added volatility with no free lunch attached.

Pro Tip: Run a stress test on every deal before closing. Model what happens to your cash flow and equity position if rents drop 15% and property values fall 10% simultaneously. If the deal survives that scenario with positive cash flow, your leverage level is defensible.

What are the key leverage metrics investors must understand?

Three ratios define how lenders and experienced investors measure leverage exposure: LTV, leverage ratio, and ICR. Knowing all three gives you a complete picture of your borrowing position.

LTV and leverage ratio

LTV equals loan amount divided by property value, with equity equal to property value minus loan balance. An 80% LTV on a $500,000 property means a $400,000 loan and $100,000 equity. Most conventional investment property lenders cap LTV at 75% to 80%, though DSCR lenders and portfolio lenders may go higher on strong cash-flowing assets. LTV defines your equity cushion and directly determines your leverage ratio.

| Metric | Definition | Example | Typical 2026 Threshold |

|---|---|---|---|

| LTV | Loan ÷ Property Value | $320K loan on $400K property = 80% | 75%–80% for most investment loans |

| Leverage Ratio | 1 ÷ (1 − LTV) | At 75% LTV: 4x leverage | 3x–5x common for buy-and-hold |

| ICR | Rental Income ÷ Annual Interest | $24K rent ÷ $16K interest = 150% | 125%–145% depending on tax status |

| DSCR | Net Operating Income ÷ Debt Service | $30K NOI ÷ $24K debt service = 1.25x | 1.20x–1.25x minimum for most lenders |

ICR and lender stress testing

The interest coverage ratio measures whether rental income covers mortgage interest by a sufficient margin. ICR thresholds in 2026 sit at 125% for basic-rate taxpayers and limited companies, and 145% for higher-rate taxpayers holding property personally. These are not suggestions. They are hard underwriting floors that determine how much you can borrow. Lenders also apply floor stress rates around 5.5% when calculating ICR, even if your actual product rate is lower. This means a deal that pencils at your note rate may not qualify at the stress rate, which is a critical distinction for portfolio planning.

Key points investors frequently miss on leverage metrics:

- ICR is calculated on interest only, not full debt service, which makes it more favorable than DSCR in some structures

- Adjusting loan structure, such as fixing the rate term, can shift stress-test calculations and increase borrowing capacity

- LTV and ICR interact: lower LTV reduces interest burden, which improves ICR and unlocks more financing

What types of leverage are commonly used in property investing?

Property investment leverage comes in several forms. Each suits a different investor profile, deal type, and risk tolerance.

| Financing Type | Best For | Key Advantage | Key Risk |

|---|---|---|---|

| Conventional Mortgage | Stabilized rentals, experienced investors | Lower rates, longer terms | Strict income documentation |

| DSCR Loan | Cash-flowing rentals, portfolio scaling | Qualified on property income, not personal income | Slightly higher rates than conventional |

| Bridge Loan | Value-add, transitional assets | Fast close, flexible terms | Short duration, higher cost |

| Hard Money Loan | Fix-and-flip, distressed acquisitions | Speed, minimal documentation | Highest cost, short term |

| Cash-Out Refinance | Equity recycling on stabilized assets | Access equity without selling | Resets amortization, increases debt load |

| HELOC | Investors with existing equity | Flexible draw, interest-only option | Variable rate exposure |

Cash-out refinancing and equity recycling

Cash-out refinancing is one of the most effective tools for scaling a portfolio without continuously adding new outside capital. Once a property appreciates or is improved, you refinance at the new value, pull out equity, and redeploy it into the next acquisition. Successful investors use refinancing cycles to recycle capital and scale portfolios without over-leveraging. The BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) formalizes this cycle. Investor MultiFamily Capital offers BRRRR strategy financing specifically structured for investors executing this model in New England and Florida markets.

A note on zero-down and creative finance

Zero-down strategies and seller financing can work for experienced investors who understand the full cost structure. For beginners, they carry serious risk. No equity means no buffer against value declines, and thin or negative cash flow under a leveraged structure can force a sale at the worst possible time. Learning how to leverage property responsibly starts with having real equity in the deal.

How can investors apply leverage strategies safely and scale their portfolios?

Safe leverage use is not about borrowing as little as possible. It is about borrowing at levels your cash flow can support under stress conditions.

-

Start with positive cash flow. Every leveraged deal must generate net rental income above all debt service, taxes, insurance, and vacancy reserves. A deal that breaks even at today’s rates fails the moment rates rise or a tenant vacates.

-

Build a reserve fund before scaling. Hold three to six months of debt service per property in liquid reserves. Lenders see this as a credit strength. More importantly, it keeps you from forced sales during market corrections.

-

Use conservative LTV on your first properties. Beginning investors should target 70% to 75% LTV. This provides equity cushion, improves ICR, and gives you room to refinance later when the property has seasoned and appreciated.

-

Stress-test every deal at floor rates. Run your ICR and DSCR calculations at a stress rate of 5.5% or higher, regardless of your actual rate. If the deal does not qualify at the stress rate, your lender will catch it anyway. Better to know before you submit.

-

Refinance strategically, not reactively. Use cash-out refinancing as a planned capital recycling event, not an emergency measure. Time refinances when valuations are strong and rates are favorable relative to your existing debt.

-

Evaluate leverage by risk-adjusted return, not just borrowing amount. Risk-adjusted return metrics give better investment decisions than simply maximizing LTV. A 65% LTV deal with strong cash flow often outperforms an 80% LTV deal with thin margins over a full market cycle.

Pro Tip: When evaluating a new market for leveraged acquisitions, check local rent-to-price ratios before modeling returns. Markets with ratios below 0.7% monthly rent to purchase price often produce negative leverage at current financing costs, regardless of appreciation potential.

Key takeaways

Leverage in property investing amplifies both returns and risks in direct proportion to your LTV, making cash flow, reserve funds, and stress-tested underwriting the three non-negotiable foundations of any leveraged portfolio strategy.

| Point | Details |

|---|---|

| Leverage ratio scales with LTV | At 80% LTV, each equity dollar controls 5x the property value, amplifying gains and losses equally. |

| ICR and DSCR are lender floors | Lenders apply stress rates around 5.5% to test affordability, not your actual product rate. |

| Cash-out refinancing scales portfolios | Equity recycling through refinancing lets investors grow without continuously adding new outside capital. |

| Positive leverage requires a spread | Your property yield must exceed your borrowing cost, or leverage destroys rather than builds returns. |

| Reserves are non-negotiable | Three to six months of liquid debt service reserves per property protects against forced sales in downturns. |

Why most investors misread leverage until it costs them

I have reviewed hundreds of deal submissions, and the most common mistake is not taking on too much debt. It is taking on debt without understanding the conditions that make it work. Investors see a low down payment as a win. What they are actually doing is maximizing their leverage ratio without stress-testing the cash flow that has to service it.

The investors who scale successfully treat leverage as a tool with specific operating conditions, not a default setting. They know their ICR before they call a lender. They model their DSCR at stress rates before they make an offer. And they treat debt approval as a starting point, not a safety signal. Getting approved for a loan does not mean the deal works under stress. It means the lender is comfortable with their exposure. Your job is to be comfortable with yours.

The investors I see build durable portfolios in markets like Massachusetts, New Hampshire, and Florida share one habit: they start conservative, learn the underwriting logic, and then scale into higher leverage positions once cash flow is proven. They also use refinancing cycles deliberately, not as a reaction to needing capital. If you are newer to leveraging equity in property, that sequence matters more than finding the highest LTV product available.

— Joe

Finance your leverage strategy with Investor MultiFamily Capital

Investor MultiFamily Capital structures financing around property cash flow, not personal income, which is exactly how leveraged investing should be underwritten.

For buy-and-hold investors, DSCR loans qualify based on rental income relative to debt service, making them the right tool for scaling a leveraged portfolio without W-2 documentation requirements. For value-add plays and transitional assets, bridge loans provide fast, flexible capital while you stabilize the property and position for a long-term refinance. Investor MultiFamily Capital serves investors across MA, NH, RI, CT, ME, and FL. Submit a Deal, Run Deal Analysis, or Apply Online to get your scenario in front of an underwriter who understands investment property leverage.

FAQ

What is leverage in property investing?

Leverage in property investing is the use of borrowed funds, typically mortgage financing, to control a property worth more than your cash investment. It amplifies both returns and losses relative to your equity contribution.

What is a good LTV for an investment property?

Most investment property lenders set maximum LTV at 75% to 80%. Conservative investors starting out should target 70% to 75% LTV to maintain an equity cushion and meet ICR thresholds under stress-rate testing.

How does ICR affect how much I can borrow?

ICR measures rental income against annual mortgage interest. Lenders require ICR of 125% to 145% calculated at a floor stress rate, often around 5.5%, which limits borrowing capacity even when your actual rate is lower.

Can you leverage investment properties using a cash-out refinance?

Yes. Cash-out refinancing lets you access accumulated equity in a stabilized property and redeploy it as a down payment on the next acquisition. This is the core mechanism behind the BRRRR strategy and controlled portfolio scaling.

What is the difference between positive and negative leverage?

Positive leverage occurs when a property’s income yield exceeds the cost of borrowing, increasing your return on equity. Negative leverage occurs when financing costs exceed the property yield, reducing returns below what an all-cash purchase would produce.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.