If you’ve been eyeing a vacation rental property and assumed you’d finance it the same way you would a long-term rental, you’re not alone. But that assumption can cost you time, deals, and money. A short-term rental loan is a specialized investment mortgage underwritten on the property’s rental income rather than your personal earnings. These loans exist because platforms like Airbnb and VRBO generate income differently than traditional leases, and most conventional lenders aren’t set up to handle that. This article breaks down exactly how short-term rental financing works, what loan types are available, and how to position yourself for approval.

Table of Contents

- Key takeaways

- What is a short-term rental loan?

- Comparing loan types for STR investors

- Approval criteria and best practices

- How to finance a short-term rental property

- My take on short-term rental financing

- Finance your next STR with Investormultifamily

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Income-based qualification | Short-term rental loans qualify borrowers on property cash flow, not W-2s or tax returns. |

| DSCR is the core metric | Lenders require a Debt Service Coverage Ratio between 1.0x and 1.25x using projected or actual rental income. |

| Multiple loan types exist | DSCR loans, bridge loans, and bank statement loans each serve different investor profiles and timelines. |

| Lenders discount projected income | Expect lenders to reduce gross rental projections by 20% to 40% when calculating your DSCR. |

| Entity formation matters | Setting up your LLC before applying prevents costly delays and satisfies most lender requirements upfront. |

What is a short-term rental loan?

A short-term rental loan is an investment property mortgage designed specifically for properties rented on platforms like Airbnb or VRBO. Unlike a conventional mortgage, which relies on your personal income to determine how much you can borrow, these loans are underwritten based on the property’s ability to generate rental revenue. The lender’s primary question is whether the property produces enough income to cover the debt payments.

The most common structure uses Debt Service Coverage Ratio underwriting. DSCR measures the ratio of a property’s net operating income to its annual debt service. DSCR requirements typically fall between 1.0x and 1.25x, meaning the property needs to generate at least as much income as the loan costs to service, and ideally 25% more. A 1.0x DSCR means income exactly covers debt payments. A 1.25x means income exceeds payments by 25%.

Here is what the standard loan parameters look like for short-term rental financing in 2026:

- Down payment: 20% to 25% of the purchase price

- Interest rates: 6.0% to 8.75%, depending on credit profile and loan type

- Minimum credit score: 640 to 720 across most lenders

- Reserves required: 6 to 12 months of mortgage payments in liquid assets

- Income source: Projected or actual short-term rental revenue from platforms or tools like AirDNA

Lenders use tools like AirDNA to estimate what a property can realistically earn based on comparable listings in the same market. For properties already operating on Airbnb or VRBO, actual platform income statements carry more weight. You can learn more about how DSCR underwriting works for investment properties before you apply.

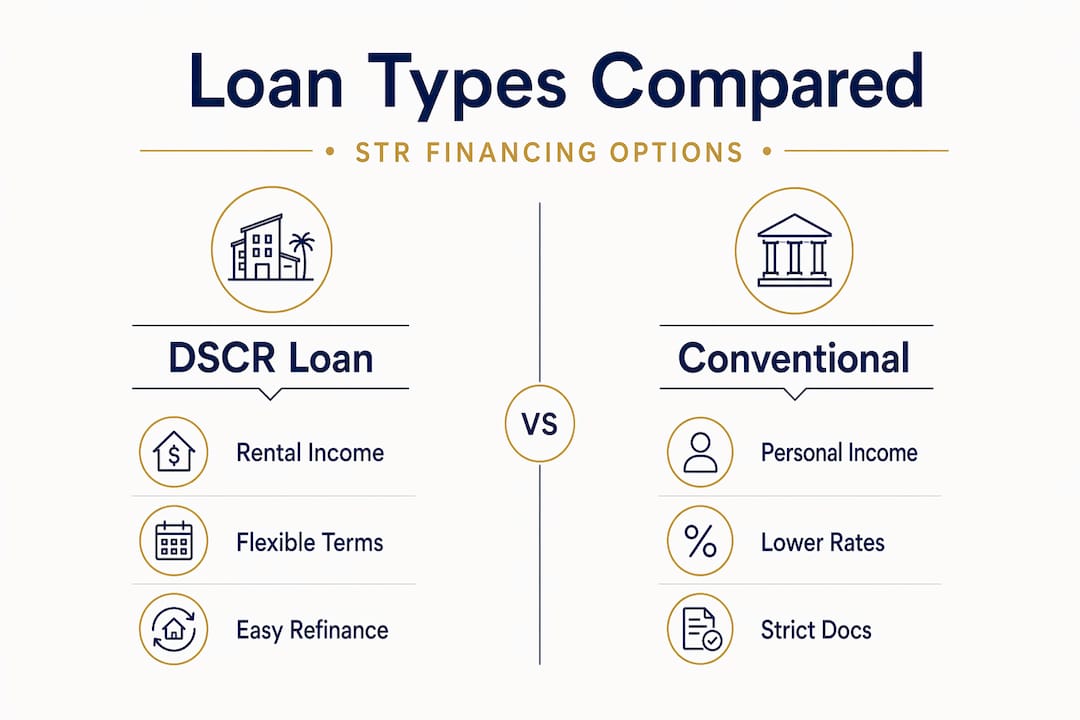

Comparing loan types for STR investors

Not every investor fits the same financing box. The right loan depends on your financial profile, investment timeline, and how the property is currently positioned.

| Loan Type | Qualification Basis | Interest Rate Range | Best For |

|---|---|---|---|

| DSCR Loan | Property rental income | 6.75% to 8.25% | Buy-and-hold STR investors |

| Conventional Mortgage | Personal income, tax returns | 5.5% to 7.0% | Owner-occupants, strict docs |

| Bank Statement Loan | 12-24 months bank deposits | 7.0% to 9.0% | Self-employed investors |

| Bridge Loan | Asset value, exit strategy | 9.0% to 12.0%+ | Quick acquisitions, rehab |

| Hard Money Loan | Asset value | 10.0% to 14.0%+ | Short-term, fast capital |

DSCR loans are the most practical option for most short-term rental investors. They allow qualification without tax returns or W-2 documentation, which matters enormously if you own multiple properties or have complex income. Closings typically run 21 to 35 days. The tradeoff is that rates run 0.5% to 1.5% higher than conventional loans, but the qualification flexibility often makes that premium worth paying.

Conventional mortgages offer lower rates but come with strict personal income documentation requirements. Most conventional lenders also limit how many financed properties you can hold, which creates a ceiling for portfolio growth.

Bank statement loans serve self-employed investors who can show consistent deposits but whose tax returns understate actual income due to deductions. These are useful but typically carry higher rates than DSCR products.

Bridge loans fund quick acquisitions or properties that need work before they qualify for permanent financing. They are based primarily on asset value and require a credible exit strategy, whether that means refinancing into a DSCR loan or selling the property. Bridge financing is expensive and carries real risk if your exit plan falls through.

Pro Tip: If you’re using a hard money or bridge loan to acquire a property, plan your refinance into a DSCR loan before you close. Refinancing hard money into a DSCR loan removes balloon payment risk and significantly reduces monthly carrying costs.

Approval criteria and best practices

Getting approved for a short-term rental loan requires more than a good credit score. Lenders are evaluating the property’s income reliability, your financial preparedness, and the overall risk of the deal. Here is what you need to address before submitting an application.

-

Model your DSCR conservatively. Lenders discount gross projected rental income by 20% to 40% to account for vacancy, seasonality, and platform fees. If AirDNA projects $60,000 in annual gross revenue, your lender may underwrite to $36,000 to $48,000. Run your own numbers at a 30% reduction minimum before you assume the deal pencils.

-

Prioritize actual income history. Verified platform income from 12 months of Airbnb or VRBO statements carries significantly more weight than third-party projections. If you’re refinancing an existing STR, gather those statements before you start the application.

-

Know your credit score position. A strong credit score improves your loan terms even when personal income isn’t part of qualification. A higher score can mean a lower rate, better LTV, or reduced reserve requirements. Aim for 700 or above to access the best pricing tiers.

-

Form your LLC before you apply. Delays in entity formation are one of the most common and avoidable causes of closing delays. Most lenders require an established LLC with a valid EIN and operating agreement. Set this up weeks before you submit a deal, not the day before closing.

-

Have a documented exit strategy. This applies especially to bridge loans. Lenders favor conservative assumptions and deals with clear repayment plans. Presenting a refinance timeline or a sale projection backed by comparable data strengthens your application significantly.

-

Prepare your reserves documentation. Most lenders require 6 to 12 months of mortgage payments in liquid reserves. Bank statements showing those funds should be ready to submit with your initial package.

Pro Tip: Avoid applying for multiple loans simultaneously. Multiple hard credit inquiries in a short window can reduce your score and signal financial stress to underwriters, even if your deal is strong.

How to finance a short-term rental property

Short-term rental financing follows a logical sequence once you understand the underwriting framework. Here is how to approach the process from deal evaluation to closing.

-

Assess income potential first. Before you make an offer, pull AirDNA data for the specific market and property type. Look at occupancy rates, average daily rates, and seasonal patterns. If the property is already operating, request 12 months of platform income statements from the seller.

-

Model DSCR with a 30% income haircut. Take your projected gross income and reduce it by at least 30%. Divide the result by your estimated annual debt service. If that ratio is 1.0x or above, the deal may qualify. If it falls below 1.0x, you either need to renegotiate the price or reconsider the acquisition.

-

Match the loan type to your investment goal. If you’re buying and holding, a DSCR loan is almost always the right structure. If you’re acquiring a distressed property to renovate and then operate as an STR, a bridge loan or fix-and-flip product gets you in the door, with a DSCR refinance as the exit.

-

Select a lender with STR experience. Not all DSCR lenders understand short-term rental income. Some apply residential underwriting logic to STR projections and come up with unreliable numbers. Work with a lender who regularly underwrites short-term rental properties and knows how to read AirDNA reports and platform statements.

-

Prepare your documentation package. This typically includes the property address, purchase contract, AirDNA report or income statements, entity documents (LLC operating agreement, EIN), and bank statements showing reserves. Having this ready before you apply compresses your timeline considerably.

-

Plan for a 21 to 35 day close on DSCR loans. This is faster than conventional financing and makes DSCR products competitive for deals with tight timelines. Bridge loans can close in as few as 7 to 14 days when needed.

The most scalable approach for building a short-term rental portfolio is to use bridge or hard money financing to acquire and stabilize properties quickly, then refinance into long-term DSCR loans once the property has operating history. That sequence gives you acquisition speed and long-term stability.

My take on short-term rental financing

I’ve worked with enough investors to say this clearly: the biggest mistake I see is optimizing for the lowest interest rate instead of the fastest, most reliable path to closing. A rate that is 0.5% lower means nothing if the loan falls apart two weeks before closing because your lender couldn’t underwrite STR income correctly.

In my experience, the investors who build successful short-term rental portfolios treat underwriting assumptions as their first line of risk management. They don’t submit deals hoping the numbers work. They stress-test the DSCR at 30% below projected income before they ever contact a lender. If the deal still pencils at that discount, it’s worth pursuing.

I’ve also seen deals collapse at the finish line because an investor hadn’t formed their LLC yet. That’s a week or more of delay that could cost you the property. Entity formation is a one-time task. Do it before you start shopping for deals, not after you’ve found one.

The other thing I’d push back on is the idea that projections are as good as history. They’re not. Lenders know it, and so should you. If you’re evaluating a property that has never operated as an STR, build in a larger margin of safety. If you can find a property with 12 months of verified Airbnb income, that operating history is worth paying a small premium for. It makes your approval faster, your terms better, and your underwriting far more defensible.

— Joe

Finance your next STR with Investormultifamily

Investormultifamily specializes in business-purpose financing for real estate investors across New England and Florida. For short-term rental investors, that means DSCR loans underwritten on actual or projected STR income, not your personal tax returns or W-2s.

Whether you’re buying your first Airbnb property in Massachusetts, scaling a vacation rental portfolio in Florida, or refinancing a hard money loan into a long-term DSCR product, Investormultifamily has the loan programs and STR underwriting experience to get your deal closed. Explore DSCR loan options built for short-term rental investors, or review the full DSCR loan program details to see if your deal qualifies. Submit your scenario today and get a same-day response.

FAQ

What is a short-term rental loan?

A short-term rental loan is an investment mortgage underwritten on the property’s rental income rather than the borrower’s personal income. Most use DSCR qualification, requiring a ratio of 1.0x to 1.25x based on projected or actual STR revenue.

How does DSCR qualification work for STR loans?

Lenders calculate DSCR by dividing the property’s net rental income by its annual debt service. They typically apply a 20% to 40% discount to gross projected income before making that calculation.

What credit score do I need for a short-term rental loan?

Most lenders require a minimum credit score of 640 to 720 for short-term rental loan approval. A score above 700 generally unlocks better rates and more favorable loan terms.

Can I use an LLC to take out a short-term rental loan?

Yes, and most lenders require it. Your LLC must be established with a valid EIN and operating agreement before you apply. Delays in entity formation are a common cause of closing delays.

What is the difference between a DSCR loan and a bridge loan for STRs?

A DSCR loan is a long-term investment mortgage based on property income, designed for buy-and-hold investors. A bridge loan is short-term financing based on asset value, used for quick acquisitions or properties that need stabilization before qualifying for permanent financing.