TL;DR:

- Construction loans for investment properties provide staged funding during building or major renovation, converting to long-term financing upon completion. Managing draw schedules, inspections, and underwriting requirements is essential for project success, with specific differences between single-close and two-close structures. Proper planning on costs, timelines, and loan terms ensures optimal outcomes for investors building rental or multifamily assets.

A construction loan for an investment property is specialized short-term financing that funds the ground-up building or major renovation of income-producing real estate, structured entirely differently from a standard purchase mortgage. Unlike a conventional loan that disburses a lump sum at closing, construction financing releases capital in staged draws tied to verified project milestones. Investors building rental properties, multifamily units, or mixed-use assets in markets like Massachusetts, Florida, or New Hampshire use these loans to control project costs while preserving liquidity. Understanding how draw schedules, lender underwriting, and loan structure interact is the difference between a project that closes on time and one that stalls mid-build.

How do construction loans for investment properties work?

A construction loan for an investment property operates in two distinct phases: the construction period, during which funds are drawn in stages, and the permanent financing phase, where the loan converts or refinances into a long-term mortgage. This two-phase structure is the defining feature of construction lending and shapes every underwriting and cash flow decision you make.

Here is how the process unfolds from closing to certificate of occupancy:

- Loan closing and initial draw. At closing, the lender commits the full loan amount but does not disburse it. The borrower receives the first draw, typically covering site preparation and foundation work.

- Draw requests tied to milestones. As construction progresses, the borrower submits draw requests supported by invoices, lien waivers, and contractor certifications. Draws are released only after a lender-ordered inspection confirms the percentage of completion matches the schedule of values.

- Interest-only payments during construction. The borrower pays interest only on the outstanding drawn balance, not the full committed loan amount. This keeps carrying costs manageable during the build.

- Lender inspections at each draw. A third-party inspector verifies work before each disbursement. Draw inspection turnaround ranges from 5 to 15 business days, which means delays in scheduling or paperwork directly delay funding.

- Conversion or refinance to permanent financing. Once construction is complete and the certificate of occupancy is issued, the loan either converts automatically to a permanent mortgage or the borrower closes a separate long-term loan.

Pro Tip: Build a 10 to 15 business day buffer into your draw schedule for each inspection cycle. Assuming same-week fund release is the most common cause of contractor payment delays on construction projects.

What are the qualification requirements for investment property construction loans?

Investment property construction loans carry stricter underwriting standards than owner-occupied construction financing because lenders bear both construction risk and investment performance risk simultaneously. Knowing what lenders evaluate before you apply prevents surprises during underwriting.

Key qualification factors include:

- Down payment and reserves. Investment construction loans typically require 25 to 30% down, with additional cash reserves to cover carrying costs if draws are delayed or construction runs over budget.

- Credit profile. Most lenders require a minimum credit score in the 680 to 720 range for investment construction financing, with stronger scores unlocking better loan-to-cost ratios.

- Builder and contractor qualifications. Lenders review the general contractor’s license, insurance, and project history. An unqualified contractor is a fast path to loan denial regardless of borrower strength.

- Project feasibility documentation. Expect to submit a full set of plans, specifications, a detailed budget, and a construction timeline. Lenders underwrite the project as much as the borrower.

- DSCR projections for permanent financing. Because rental income cannot be used for qualification during the construction phase, lenders model projected rents against the permanent loan’s debt service. A DSCR of 1.25 or higher is the standard target for favorable pricing on the permanent loan.

- Loan-to-cost and loan-to-value ratios. Lenders cap loan-to-cost (LTC) at 70 to 80% of total project cost and loan-to-value (LTV) at 65 to 75% of completed appraised value. Both ratios must be satisfied simultaneously.

Pro Tip: Prepare a pro forma rental analysis before your first lender conversation. Lenders underwriting the permanent phase want to see that projected rents cover debt service at a DSCR of at least 1.0, and preferably 1.25, before they commit to the construction loan.

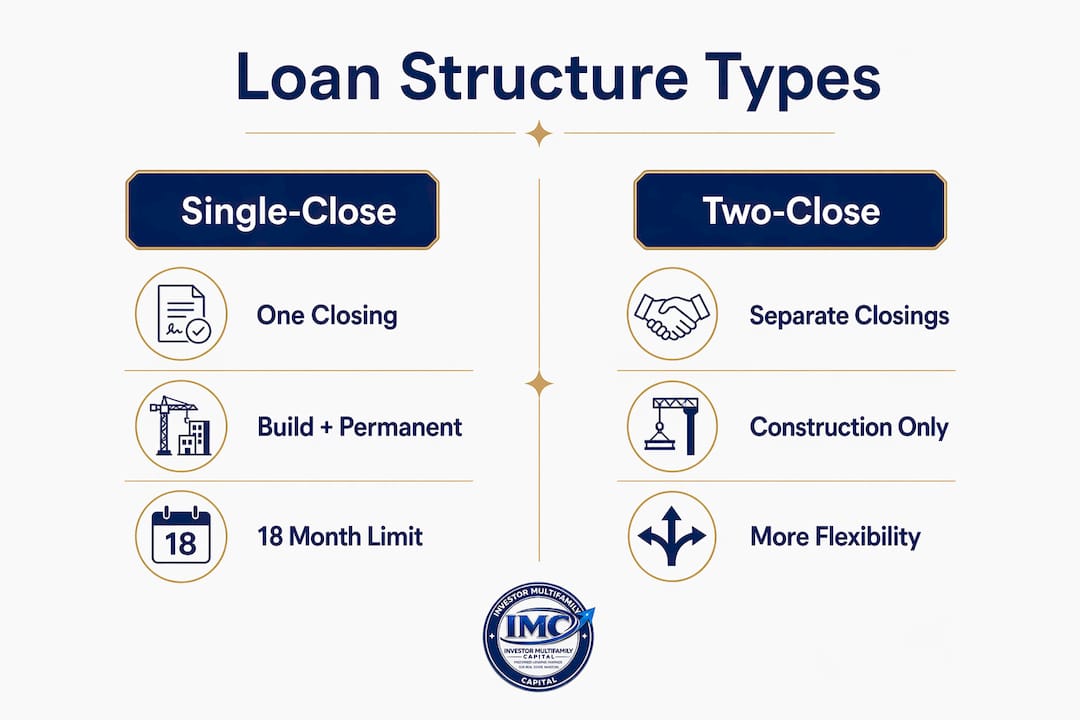

Single-close vs. two-close construction loans: which structure fits investors?

The choice between a single-close and a two-close construction loan is one of the most consequential structural decisions in investment property financing. Each approach carries distinct underwriting implications, cost profiles, and timeline constraints.

| Feature | Single-close | Two-close |

|---|---|---|

| Number of closings | One closing covers both phases | Separate closings for construction and permanent loan |

| Timeline limits | Maximum 18 months total construction; no single period over 12 months | More flexible; timeline set by lender and project scope |

| Closing costs | Lower overall; one set of closing costs | Higher overall; two full sets of closing costs |

| Rate lock | Rate locked at initial closing | Permanent loan rate set at second closing, subject to market conditions |

| Re-underwriting risk | Minimal if timeline is met | Full re-underwriting at second closing |

| Best for | Projects with firm timelines and predictable scopes | Complex builds, phased projects, or uncertain timelines |

Single-close loans reduce paperwork and lock in permanent financing terms upfront, but exceeding the 18-month construction window voids the streamlined conversion and can trigger costly re-underwriting. Two-close loans add a second set of closing costs and expose the borrower to rate risk at the permanent closing, but they give experienced investors the flexibility to manage complex or phased construction schedules without hard deadline pressure.

For most ground-up rental property builds in New England or Florida with a defined scope and experienced contractor, a single-close structure is the more cost-efficient path. For multifamily projects with phased delivery or adaptive reuse conversions, two-close financing is the more practical choice.

How to manage construction costs, draw schedules, and avoid funding delays

Cash flow gaps during construction are rarely caused by contractor slowdowns. Draw funding depends more on the completeness of paperwork and inspection scheduling than on actual construction progress. Investors who treat draw management as an administrative afterthought routinely face two to three week funding delays that compound across a six-month build.

The following practices keep draws on schedule and costs under control:

- Build your schedule of values (SOV) with precision. The SOV is the master budget document that ties each draw to a specific scope of work. Vague line items like “framing” without square footage or unit counts create disputes at inspection time.

- Submit draw packages early and completely. Each draw request should include updated invoices, conditional lien waivers from all subcontractors, a completed draw request form, and photos of completed work. Missing any single document restarts the clock.

- Anticipate the S-curve draw pattern. Draw schedules follow an S-curve: slower initial draws during sitework and foundation, peak draws during framing and mechanical installation, and tapering draws during finishes. Model your cash flow accordingly, not as a straight line.

- Track change orders in real time. Every approved change order must be documented and submitted to the lender before the affected work begins. Unapproved scope changes are not fundable.

- Model interest reserves accurately. Interest accrues only on drawn funds, not the full loan commitment. The average outstanding balance over a construction period typically runs 55 to 65% of the total loan, which means your interest reserve budget should reflect that curve, not the full loan amount from day one.

| Draw phase | Typical % of total loan | Primary work covered |

|---|---|---|

| Draw 1 | 10 to 15% | Site prep, foundation |

| Draw 2 to 3 | 35 to 45% | Framing, roofing, mechanicals |

| Draw 4 to 5 | 25 to 35% | Insulation, drywall, finishes |

| Final draw | 10 to 15% | Punch list, certificate of occupancy |

Pro Tip: Open a dedicated project operating account and fund it with your interest reserve and contingency budget before construction starts. Mixing project funds with operating capital is the fastest way to lose visibility on where your money is going.

How to evaluate if a construction loan fits your investment strategy

Building from the ground up is not always the right move, even when financing is available. A construction loan for a rental property makes sense in specific market and portfolio conditions. Investors should run this evaluation before committing to a ground-up project.

- Compare total cost to buy versus build. In supply-constrained markets like coastal Massachusetts or South Florida, building new can deliver a property at below-replacement cost relative to existing inventory. In markets with abundant existing rental stock, the cost and timeline premium of new construction rarely pencils out.

- Quantify the rental income delay. A 12 to 18 month construction period means 12 to 18 months of zero rental income while carrying costs accumulate. Model that gap explicitly against the projected stabilized cash flow to confirm the project’s net present value is positive.

- Evaluate DSCR at permanent loan terms. Use DSCR loan benchmarks to stress-test the permanent financing phase. If projected rents produce a DSCR below 1.0 at current rates, the project does not support its own debt service and requires renegotiation of scope, cost, or rent assumptions.

- Assess design and specification control. New construction gives investors full control over unit mix, finishes, and systems. That control has real value in markets where tenants pay premiums for modern units, and it eliminates deferred maintenance risk from day one.

- Consider supplemental financing tools. A bridge loan can cover the gap between construction completion and permanent financing stabilization. Some investors also use cash-out refinances on existing portfolio properties to fund equity contributions on new construction deals.

Key takeaways

A construction loan for an investment property succeeds when draw management, underwriting preparation, and permanent financing strategy are planned together before the first shovel hits the ground.

| Point | Details |

|---|---|

| Two-phase loan structure | Construction draws convert or refinance to permanent financing once the certificate of occupancy is issued. |

| Down payment requirements | Investment construction loans require 25 to 30% down plus cash reserves for carrying costs and contingencies. |

| Draw inspection timing | Lender inspections take 5 to 15 business days per draw; build this into your project schedule to avoid cash flow gaps. |

| DSCR benchmark for permanent loan | Target a DSCR of 1.25 or higher on projected rents to qualify for favorable permanent financing terms. |

| Single-close vs. two-close | Single-close saves costs but caps construction at 18 months; two-close adds flexibility at the cost of a second closing. |

What I’ve learned from watching construction deals succeed and fail

From where I sit, the investors who run into serious trouble on construction projects are almost never undercapitalized at the start. They run into trouble because they underestimated the administrative load of draw management and treated lender inspections as a formality rather than a critical path item.

The 5 to 15 business day inspection window is not a suggestion. It is a hard operational constraint that compounds across every draw cycle. On a six-draw project, that is potentially 90 business days of inspection time built into the schedule before a single delay occurs. Investors who do not model that reality end up paying contractors out of pocket to keep crews on site while waiting for fund releases.

The other pattern I see consistently is investors choosing single-close construction loans on projects with optimistic timelines. The 18-month hard cap from Fannie Mae guidance is not negotiable. When a project slips to month 20 because of permitting delays or supply chain issues, the streamlined conversion disappears and re-underwriting fees follow. Two-close loans cost more upfront but eliminate that specific risk entirely on complex builds.

My practical advice: work with a loan officer who has closed at least five investment construction deals, not just residential construction loans. The underwriting logic, draw administration, and permanent financing coordination are different enough that experience in consumer construction lending does not transfer cleanly to investment property financing.

— Joe

Build your next investment property with Investor MultiFamily Capital

Investor MultiFamily Capital structures ground-up construction loans and multifamily financing for real estate investors across New England and Florida. Whether you are building a two-unit rental in Massachusetts, a multifamily project in Connecticut, or a new construction income property in Florida, Investor MultiFamily Capital underwrites based on project feasibility and property cash flow, not personal income. DSCR loan programs are available for the permanent financing phase, giving investors a clear path from ground-break to stabilized asset. Submit a Deal or Run Deal Analysis to get your construction scenario in front of an experienced investment property lender today.

FAQ

What is a construction loan for an investment property?

A construction loan for an investment property is short-term financing that funds the building of income-producing real estate in staged draws tied to verified construction milestones, then converts or refinances to a permanent mortgage at project completion.

How much do you need down for an investment property construction loan?

Investment property construction loans typically require a down payment of 25 to 30% of total project cost, plus cash reserves to cover carrying costs and contingencies during the construction period.

Can rental income be used to qualify for a construction loan?

Rental income cannot be used for loan qualification during the construction phase because the property is not yet income-producing. Lenders underwrite the borrower’s financial strength and project feasibility instead, then model projected rents for the permanent loan phase.

What is the difference between a single-close and two-close construction loan?

A single-close loan combines construction and permanent financing into one closing with a maximum 18-month construction period, while a two-close loan uses separate closings for each phase, offering more timeline flexibility at the cost of additional closing expenses.

What DSCR do lenders require for investment construction loans?

Lenders typically require a minimum DSCR of 1.0 for loan qualification, with a DSCR of 1.25 or higher as the target for favorable pricing on the permanent financing phase of an investment construction loan.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.