TL;DR:

- A multifamily property has two or more self-contained housing units with independent facilities and entrances. Properties with two to four units qualify for residential financing, while five or more units require commercial loans with different standards. Verifying legal unit count and permits is essential to avoid costly financing and classification issues.

A multifamily property is a residential building or complex containing two or more self-contained housing units, each with its own kitchen, bathroom, and private entrance. This definition covers everything from a duplex on a quiet street in Providence to a 300-unit apartment tower in Miami. Understanding what counts as multifamily property is the first step every real estate investor must take before evaluating deals, securing financing, or planning an exit. The classification determines your loan type, down payment requirement, underwriting method, and long-term tax treatment.

What counts as multifamily property: core definition and types

A multifamily property definition starts with two requirements: two or more separate housing units and full independent living facilities in each unit. A single-family home with a detached garage does not qualify. A house with a finished basement that shares a kitchen with the main floor does not qualify either. The unit count and the independence of each unit are both required.

The most common types of multifamily properties break down by scale and structure.

| Property Type | Unit Count | Structural Notes |

|---|---|---|

| Duplex | 2 | Side-by-side or stacked units, shared wall |

| Triplex | 3 | Three attached units, one owner common |

| Quadruplex (4-plex) | 4 | Four units, last tier of residential financing |

| Garden apartment | 5–50 | Low-rise, surface parking, outdoor access |

| Mid-rise apartment | 50–200 | Elevator building, 4–12 floors |

| High-rise apartment | 200+ | Institutional scale, professional management required |

Structural differences in multifamily properties directly affect operating expenses and management complexity. A duplex owner handles two sets of appliances and two rooflines. A mid-rise operator manages elevators, common areas, and a full maintenance staff. The physical structure of a property shapes its cash flow profile before a single rent check arrives.

Pro Tip: Walk the property and count every exterior entrance before closing. Each door that leads to a fully independent unit is a data point that affects your loan classification and your insurance policy.

How is a multifamily property classified for financing?

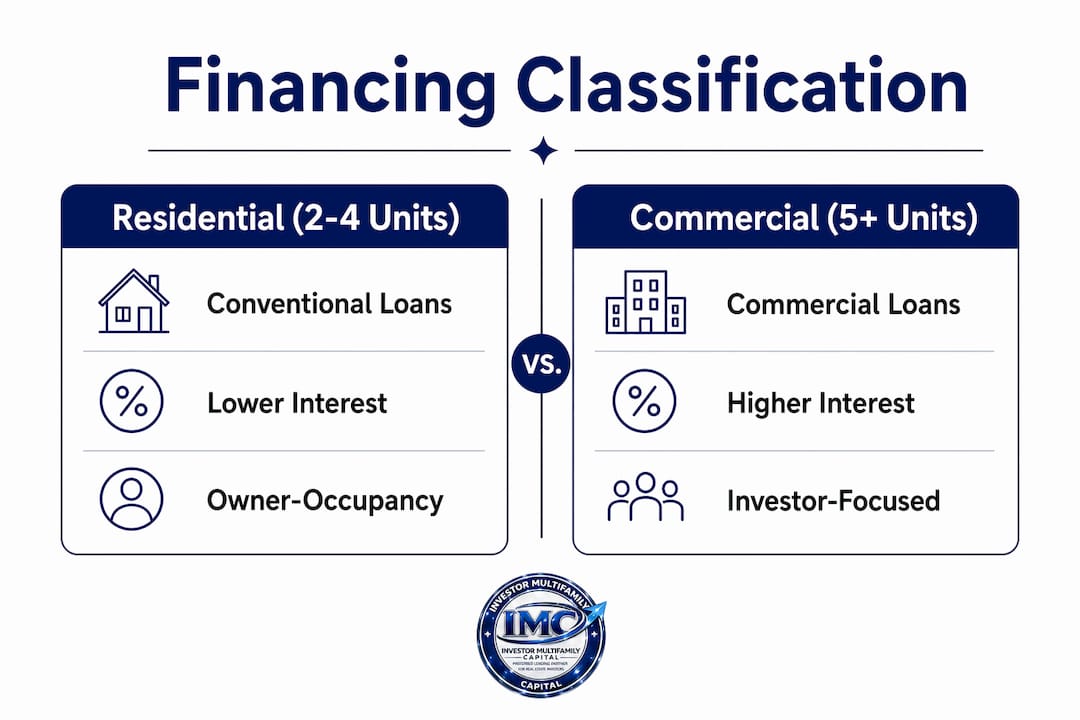

The four-unit threshold is the most consequential line in real estate finance. Properties with 2–4 units are classified as residential and qualify for conventional loans. Properties with five or more units are commercial real estate and require commercial financing with entirely different underwriting standards.

This distinction changes nearly every term in your loan.

| Feature | Residential (2–4 units) | Commercial (5+ units) |

|---|---|---|

| Loan classification | Residential mortgage | Commercial real estate loan |

| Down payment | 3.5%–10% | 20%–30% |

| Underwriting basis | Borrower income and credit | Net operating income (NOI) |

| Valuation method | Comparable sales | Income capitalization |

| Loan structure | Fully amortizing | Often balloon structure |

Owner-occupancy does not override the five-unit commercial rule. An investor who plans to live in one unit of a six-unit building still needs a commercial loan. That surprises many first-time investors who assume occupancy changes the classification. It does not.

Local zoning and assessor methodology can also override unit-count-based classification. A four-unit building in a commercially zoned district may face different tax treatment and compliance requirements than an identical building in a residential zone. Always verify zoning before you underwrite a deal, not after.

Investors targeting multifamily financing options should map out which classification applies before approaching any lender. The loan product, the required reserves, and the approval timeline all depend on it.

What qualifies as a multifamily unit legally?

Each unit in a multifamily property must meet specific habitability criteria to count as an independent dwelling for lending and legal purposes. A qualifying unit requires its own kitchen, bathroom, and private entrance, plus valid permits confirming the space was legally converted or constructed as a separate unit.

Investors frequently encounter four problem scenarios during due diligence:

- Unpermitted basement apartments. A finished basement with a kitchen and bathroom may look like a unit. Without a certificate of occupancy and proper egress, lenders will not count it. The property reverts to a lower unit count for financing purposes.

- In-law suites. An attached suite with a private entrance but a shared kitchen does not meet the independent unit standard. It is an accessory space, not a multifamily unit.

- Accessory dwelling units (ADUs). A detached ADU with full facilities can qualify as a separate unit, but only if local permits confirm it as a legal dwelling. Unpermitted ADUs carry the same risk as unpermitted basements.

- Shared entrance conversions. A large Victorian home divided into apartments but sharing a single front door may fail the private entrance test depending on local code and lender guidelines.

Non-conforming units can force a property into more expensive commercial loans or disqualify it from financing entirely. A seller who claims a property is a triplex but cannot produce permits for the third unit is presenting a two-unit property for financing purposes.

Pro Tip: Pull the certificate of occupancy and the town assessor’s card before making an offer. Both documents confirm the legal unit count and flag any unpermitted work that could derail your financing.

Investment considerations tied to multifamily classifications

The 2–4 unit range is the entry point for most new real estate investors. Residential financing terms, lower down payments, and simpler underwriting make small multifamily properties accessible without institutional capital. The scale benefits of multiple income streams exist without the operational complexity of a commercial asset.

Four investment considerations stand out across the classification spectrum:

-

Financing access. A duplex or triplex qualifies for residential loan products with lower down payments and income-based underwriting. A six-unit building requires commercial financing, higher reserves, and NOI-based approval. The loan type shapes your cash-on-cash return from day one.

-

Vacancy risk. A single-family rental goes to zero income when vacant. A four-unit property at 75% occupancy still generates three rents. Diversified income streams reduce the financial impact of any single vacancy.

-

Management complexity. Large multifamily communities with 200 or more units are generally institutionally owned and require professional management and compliance frameworks. Smaller properties are often managed by individual operators. The jump from a four-unit to a ten-unit property is not just a unit-count increase. It is a shift in operational demands.

-

Scale and exit strategy. A four-unit property sells to both investors and owner-occupants, which broadens your buyer pool at exit. A ten-unit building sells only to investors, which narrows it. That difference affects your hold period and your exit pricing.

Structural classification is more critical than just unit count when assessing investment risk and management scope. A 12-unit garden apartment complex and a 12-unit mid-rise have the same unit count but very different maintenance profiles, insurance costs, and management demands.

Investors evaluating loan options for multifamily deals should model both the residential and commercial scenarios before committing to a purchase price. The financing structure changes the numbers materially.

Key Takeaways

Multifamily property classification hinges on two factors: unit count and the legal independence of each unit, with the four-unit threshold determining whether residential or commercial financing applies.

| Point | Details |

|---|---|

| Core definition | Two or more units, each with its own kitchen, bathroom, and private entrance. |

| Four-unit threshold | Properties with 2–4 units use residential financing; five or more units require commercial loans. |

| Legal unit requirements | Each unit needs permits, proper egress, and fully independent facilities to count for financing. |

| Investment entry point | The 2–4 unit range offers residential loan terms and lower barriers for new investors. |

| Zoning matters | Local zoning and assessor classification can override unit-count rules and affect financing. |

The four-unit line is where most investors make their biggest mistake

The four-unit threshold sounds simple until you are standing in front of a property that straddles it. I have seen investors buy what they believed was a four-unit building, only to discover during underwriting that one unit lacked a certificate of occupancy. The lender counted three units. The residential loan they planned on evaporated, and the deal had to be restructured as a commercial loan with a 25% down payment instead of 10%.

The lesson is not to avoid five-unit properties. The lesson is to verify the legal unit count before you negotiate price or structure your financing. Pull permits. Talk to the local building department. Read the assessor’s card. These steps take a few hours and can save you from a complete deal restructuring at the closing table.

The other mistake I see regularly is investors who cross the five-unit line without understanding what commercial underwriting actually requires. NOI-based approval means the property’s income must support the debt on its own. If rents are below market or the building has deferred maintenance, the NOI may not qualify even if you personally have strong credit and cash reserves. That is a fundamentally different risk profile than residential lending.

For investors in New England and Florida, the local market adds another layer. Zoning in older Massachusetts mill towns or Connecticut coastal communities can be inconsistent. A building that looks residential may sit in a mixed-use zone that triggers different treatment. Always verify locally, not just at the state level.

The sweet spot for most investors building their first portfolio is the 2–4 unit range. Residential financing terms, manageable operations, and a broader exit market make these properties the most forgiving place to learn the business. Once you understand how the classification system works, scaling into commercial multifamily becomes a deliberate choice rather than an accidental one.

— Joe

Financing multifamily deals with Investor MultiFamily Capital

Investor MultiFamily Capital provides business-purpose financing for real estate investors across New England and Florida, covering the full range of multifamily property classifications.

For residential multifamily deals in the 2–4 unit range, DSCR loan products qualify based on property cash flow rather than personal income. For commercial multifamily assets at five or more units, Investor MultiFamily Capital structures deals around NOI and asset performance. Investors in Massachusetts can access multifamily financing in MA tailored to local market conditions. Submit a Deal or Apply Online to run your scenario with a lender that underwrites to the property, not your W-2.

FAQ

What is the minimum unit count for a multifamily property?

A multifamily property requires at least two separate housing units. Each unit must have its own kitchen, bathroom, and private entrance to qualify.

Does a duplex count as multifamily?

Yes. A duplex contains two independent units and meets the multifamily property definition for both financing and classification purposes.

What is the difference between residential and commercial multifamily?

Properties with 2–4 units are residential multifamily and qualify for conventional loan products. Properties with five or more units are commercial real estate requiring commercial financing with NOI-based underwriting and higher down payments.

Can an in-law suite count as a multifamily unit?

No. An in-law suite that shares a kitchen or lacks a fully private entrance does not meet the independent unit standard. It does not count as a separate unit for financing or legal classification.

Does zoning affect multifamily property classification?

Yes. Local zoning and assessor methodology can override unit-count-based classification. A four-unit building in a commercial zone may face different financing treatment and tax obligations than the same building in a residential zone.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.

Recommended

- What Is Multifamily Financing? A 2026 Investor Guide | Investor MultiFamily Capital

- Investor Financing Insights | Investor MultiFamily Capital Blog

- Construction Loan Investment Property: 2026 Investor Guide | Investor MultiFamily Capital

- Investment Property Loan Options for Real Estate Investors | Investor MultiFamily Capital